Page Contents

All about job work in GST

Job work in GST is an outsourced activity undertaken by the principal that may or may not culminate into manufacture. For example, An automobile company sends spare parts to a job worker for coating. Coating here is an outsourced activity performed by a third party.

Define Job Work?

Section 2(68) of the CGST Act defines ‘Job work’ as ‘‘any treatment or process undertaken by a person on goods belonging to another registered person”.

Who is a job worker and who is a principal?

The person who undertakes the job of treatment or process for another person is a job worker. The owner of the goods who engages the job worker is called the Principal.

Whether the ownership of the goods get transferred when the goods are transferred? The ownership of the goods remains with the principal.

What is the time limit for the return of processed goods?

According to Section 19 of the CGST Act, Input goods should be brought back with one year and Capital goods should be brought back within three years.

Further, the provision of return of goods is not applicable in the case of molds and dies, jigs, and fixtures or tools supplied by the principal to the job worker.

What if goods are not received back within the stipulated time?

If the goods are not sold or brought back within the stipulated time, the supply between the Principal and the worker is treated as “Deemed Supply” and tax is payable thereon.

What are Job work procedural aspects?

A principal can send input or capital goods under intimation and subject to certain conditions without payment of tax to a job worker and from there to another job worker and after completion of job work bring back such goods without payment of tax.

The principal is not required to reverse the ITC availed on inputs or capital goods dispatched to job workers.

A principal can send inputs or capital goods directly to the job worker without bringing them to his premises.

Still, the principal can avail the credit of tax paid on such inputs or capital goods.

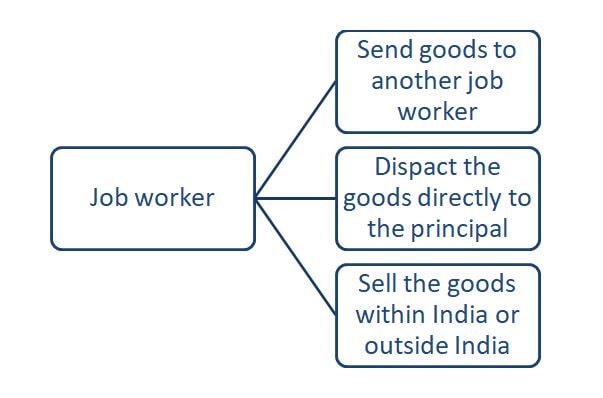

What are options available to Job workers after processing goods?

A job worker has three options available after working on the principal goods.

- Send the goods to another job worker for further processing.

- Dispatch the goods to the principal place of business without payment of tax.

- Remove the goods on payment of tax within India or without payment of tax for export outside India.

Can goods be sold directly from the Job worker’s premises by the principal?

The principal can supply goods from the place of business of the job worker if the principal declares the place of business of the job worker as the additional place of business. If the job worker is registered under Section 25 then no need to declare an additional place of business.

How goods are transported in the case of job work?

In the case of the job work, goods are transported via Delivery Challan. Delivery Challan in the prescribed format is required for the transportation of goods from one place to another under GST in case of Job work.

What are the contents of Delivery Challan?

- Date of issuing challan and date of actual transportation

- Details about consignor and consignee like Name, address, and GSTIN

- Description, HSN code, and Quantity of Goods

- Basic value, tax rate, and tax amount.

- Place of supply and signature.

The challan should always be serially numbered.

Whether Input Credit on goods supplied to job worker can be claimed?

Section 19 of CGST Act, 2017 provides that the person supplying taxable goods to the job worker shall be entitled to take input credit of tax paid on inputs sent to the job worker.

What is the treatment of waste generated by the Job worker?

According to Section 143 (5) of the CGST Act, 2017, waste generated at the place of the job worker may be supplied directly by the registered job worker from his place of business on payment of tax otherwise such waste may be cleared by the principal, in case the job worker is not registered.

Connect with us at +917701879108 and gstmentor1@gmail.com