M: +917701879108 E: gstmentor1@gmail.com

GST returns (GSTR-1 and GSTR-3B) online filing services

GST Returns are mandatorily required to be all types of GST-registered persons. GST Returns (GSTR-1 and GSTR-3B) are filed online by us. We have categorized our plans on the basis of turnover which is as follows. Three months’ packages have been provided below.

Basic Package

3 Months Accounting and GST Returns for entities having turnover up to Rs. 10 Lakhs

Rs. 1999

- GSTR-1 Filling

- GSTR-3B filling

- TDS/TCS Statement for Ecommerce Sellers

- Accounting, Purchase and Sales Register & Preparing Inventory Records

- Input Tax Credit & GSTR 2A Reconcillation

- GST Consultant 24/7 support

- GST Payment Support

Standard Package

3 Months Accounting and GST returns for entities having turnover from Rs. 10 Lakhs to Rs. 50 lakhs

Rs. 2499

- GSTR-1 Filling

- GSTR-3B Filling

- TDS/TCS Statement for E-commerce Sellers

- Accounting, Purchase and Sales Register & Preparing Inventory Records

- Input Tax Credit & GSTR 2A Reconcilation

- GST Consultant 24/7 Support

- GST Payment Support

Premium Package

3 Months Accounting and GST Returns for entities having turnover exceeding Rs. 50 Lakhs to 1 crore

Rs. 3749

- GSTR-1 & GSTR-3B Filing

- TDS/ TCS Statement for E-commerce Sellers

- Accounting, Purchase and Sales register & Preparing Inventory Records

- Vendor Reconcilation

- Input Tax Credit & GSTR 2A Reconcilation

- GST Payment Support

- Payment Reconcilations for E-commerce

-

+917701879108 // +918588918033

-

gstmentor1@gmail.com

What are the types of GST Returns and their due dates?

| Return form | Description of form | Frequency | Due date |

|---|---|---|---|

|

GSTR-1

|

Details of outward supplies of taxable goods and/or services affected. |

Monthly and Quarterly (If opted under the QRMP scheme) |

11th of next month and 13th of the month succeeding the quarter for QRMP scheme |

|

IFF (Optional by taxpayers under the QRMP scheme)

|

Details of B2B supplies of taxable goods and/or services affected.

|

Monthly (for the first two months of the quarter) |

13th of the next month.

|

|

GSTR-3B

|

Summary return of outward supplies and input tax credit claimed, along with payment of tax by the taxpayer.

|

Monthly and Quarterly (For taxpayers under the QRMP scheme) |

22nd or 24th of the month succeeding the quarter*** |

|

CMP-08

|

Statement-cum-challan to make a tax payment by a taxpayer registered under the composition scheme under Section 10 of the CGST Act. |

Quarterly |

18th of the month succeeding the quarter. |

|

GSTR-4 |

Return for a taxpayer registered under the composition scheme under Section 10 of the CGST Act.

|

Annually |

30th of the month succeeding a financial year. |

|

GSTR-5

|

Return to be filed by a non-resident taxable person.

|

Monthly

|

20th of the next month.

|

|

GSTR-5A

|

Return to be filed by non-resident OIDAR service providers.

|

Monthly

|

20th of the next month.

|

|

GSTR-6

|

Return for an input service distributor to distribute the eligible input tax credit to its branches.

|

Monthly

|

13th of the next month

|

|

GSTR-7 |

Return to be filed by registered persons deducting tax at source (TDS).

|

Monthly

|

10th of the next month.

|

|

GSTR-8

|

Return to be filed by e-commerce operators containing details of supplies effected and the amount of tax collected at source by them.

|

Monthly

|

10th of the next month.

|

|

GSTR-9

|

Annual return by a regular taxpayer.

|

Annually

|

31st December of the next financial year.

|

|

GSTR-9C |

Self-certified reconciliation statement.

|

Annually

|

31st December of the next financial year.

|

|

GSTR-10

|

Final return to be filed by a taxpayer whose GST registration is cancelled.

|

Once, when the GST registration is cancelled or surrendered.

|

Within three months of the date of cancellation or date of cancellation order, whichever is later.

|

|

GSTR-11

|

Details of inward supplies to be furnished by a person having UIN and claiming a refund

|

28th of the month following the month for which statement is filed.

|

GSTR-11

|

|

ITC-04 |

Statement to be filed by a principal/job-worker about details of goods sent to/received from a job-worker

|

Annually for aggregate turnover upto INR 5 crores and halfyearly for aggregate turnover exceeding INR 5 crores. |

25th April where aggregate turnover is up to Rs.5 crore and 25th October and 25th April where aggregate turnover exceeds Rs.5 crore. |

What are the consequences of not filing GST Returns?

-

Issue of show cause notice

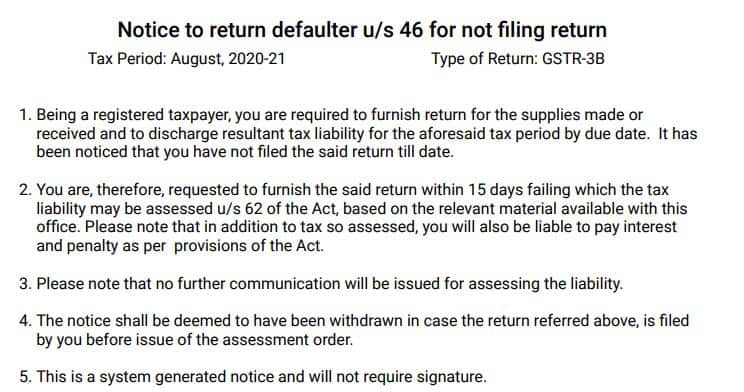

GST common portal will issue a notice under Section 46 of CGST Act, 2017 for not filing return. Under the notice, timelimit will be provided and in case of consecutive failure to file return tax liability would be determined under Section 62 of CGST Act, 2017 and an order would be passed demanding tax liability along with penalty and interest.

-

Suo moto GST Registration cancellation

Consecutive non filing of GSTR-1 and GSTR-3B for the period extending to more than six months will lead to cancellation of GST registration. Further, notice and order would be issued demanding the tax liability if any. The GST registration cancellation would not be revoked unless the applicable returns are filed by the taxpayer. Even if in future taxpayer tries to obtain new GST registration, GST officer will ask to clear the penalty dues of previoous GST registration so obtained.

-

GST Input tax credit would not be transferred to customers

Non filing of GSTR-1 (Return for outward supplies) will lead to dispute with customers as GST levied on our sales invoices will not be transferred to registered person leading to disputes and payment blocking by the customers. It will bring disrepute to the business.

-

Interest would be levied on outward supplies

Interest on net tax liability (GST to be paid on outward supplies less GST input credit available) would be calculated automatically by GST portal at the time of filing return for delay in filing of GSTR-1 and GSTR-3B.

-

Late fees would be levied

Late fees would be levied on delay in filing of GSTR-1 and GSTR-3B which will actas additional burden on taxpayer.

-

GST TCS would not get transferred to seller on ecommerce

GST TCS collected by ecommerce operators would not get transferred in electronic cash ledger in case GSTR-6 is not filed by ecommerce operator. This will lead loss of trust of seller with ecommerce operator as it will be a direct burden upon the seller supplying goods and services through ecommerce operator.

Notice issued for not filing GSTR-3B within the proper timeline

What is Zero return or Nil GSTR-1 and GSTR-3B filing?

Taxpayers normally forget or are unaware of filling out GST Returns after obtaining GST Registration. The penalty of INR 20 per day is levied in case Nil Return is not filed even if the business is not started. For example, ABC Limited applied for GST registration on 15 July and obtained a registration certificate on 18 July. Whether it needs to file a return for the month of July or directly start from August? GST returns start from the date of registration and here effective date of registration is 18 July, so for GSTR-1 the due date of filing would be the 11th of August and for GSTR-3B, it would be the 20th of August.

We need to understand whether a return would be filed in all cases even if there are no sales and purchases. Yes, Even if there is no output tax or Input Tax credit, the Return shall still be filed and that would be your “Nil Return”.

Description of GST Returns filed by various taxpayers in detail

GST Returns are mandatory to be filed for each and every registered person. Whether it is a company, partnership, HUF, or an individual proprietor. Under GST Returns have been specified separately for different types of entities which are as follows.

GSTR-1/IFF By Regular Persons

GSTR-1 return is a detail of outward supplies filed by every registered person other than Composite Taxpayer, Non-resident taxable person, Input Service Distributor, Person deducting Tax collected at Source, E-commerce operators like Amazon and Flipkart.

The due date of GSTR-1 depends upon the turnover of the business. Businesses with sales up to 1.5 crores have the option to file return quarterly basis while turnover more than 1.5 crore file returns on monthly basis.

Turnover More than 1.5 Crores: From October 2020 to March 2021, the due date of GSTR-1 is the 11th of the next month.

Turnover Less than 1.5 Crores: For the Quarter October 2020 to December 2020 GSTR-1 due date was the 13th of January and for January 21 to March 21 quarter due date is the 13th of April. This is due to the launch of the Invoice Furnishing facility in the QRMP scheme.

GSTR-3B By Regular Persons

GSTR-3B is the most important return. In this return only tax liability is paid which is shown in GSTR-1 and Input tax credit is claimed.

It is required to be filed by every registered person other than Supplier of OIDAR services, Composition taxpayer, Non-resident taxable person, Input Service Distributor, Persons deducting TCS, and E-commerce operator.

It is filed monthly or for a part of a month. Even if no supplies are affected during that month or there is no claim of Input Tax Credit a “Nil Return” shall still be filed as we discussed above.

However, initially, GST-3 was decided as a payment return. Since it is not operating still now a rule was added to consider GSTR-3B as GST-3 payment return.

GSTR-3 B’s due date used to be the 20th of next month. However, states have established their own rules on the basis of turnover now.

GSTR-4 By Composition Taxpayers

Composition Taxpayers or persons who are availing the benefits of Notification 02/2019 stating Composition Scheme for a supplier of services with a tax rate of 6% having annual turnover in the preceding year up to Rs. 50lakhs,

are required to file a yearly return for the entire year or part thereof.

The due date of filling is GSTR-4 for composition dealers is 30th April following the end of such financial year.

However, Composition taxpayers are required to furnish a statement every quarter or a part containing details of self-assessed tax in Form CMP-08 till the 18th day of the month succeeding such a quarter.

GSTR-5 By Non Resident Taxable Persons

A Non-resident taxable person under GST is the one who occasionally undertakes transactions involving the supply of goods and services or both whether as principal or agent or in any other capacity but who has no fixed place of business or residence in India.

They are required to file GSTR-5 Return monthly or for a part of the month. The due date for such return is the 20th of the next month or the seventh day after the last day of validity of registration whichever is earlier.

They are not required to file an annual return.

GSTR-5A By OIDAR's

Online Information Database Access and Retrieval Services (OIDAR) are those services that are provided through the medium of the internet and received online without any physical interface like providing advertisement online, Cloud Services, or even downloading an E-book.

OIDAR are required to file GSTR-5A monthly or for a part of a month and the due date for such return is the 20th of next month.

GSTR-6 By Input Service Distributors

An Input Service Distributor means an office of the supplier of goods or services or both which receives tax invoices issued under Section 31 towards the receipt of Input Services and issues prescribed document for the purpose of distributing the Input Credit to a supplier of taxable goods or services having the same PAN number as that of office.

Input Service Distributors are required to file GSTR-6 monthly or for a part of the month and the due date for such return is the 13th of next month.

GSTR-7 By Persons deducting TDS

Every registered person who deducts TDS is required to file form GSTR-7 monthly or for a part of the month and the due date for such return is the 10th of the next month.

GSTR-8 By Ecommerce Operators

E-commerce operators are required to deduct Tax Collected at source for all eCommerce sellers and such TCS collected is filed via GSTR-8 return.

E-commerce Operators are required to file GSTR-8 monthly or for a part of the month and the due date for such return is the 10th of the next month.

GSTR-9 Annual Returns

Filed by registered taxpayers except for Nonresident taxable persons. Input Service Distributors, Persons deducting TDS, E-commerce Operators, Casual Taxable person.

The due date set for this return is 31st December of next financial year which has been extended earlier in most years.

It is an annual return and along with it, GSTR-9c is required to be filed for taxpayers having turnover more than 5 crores for FY 2018-19 and 2019-20.

Even if it is not filed, it will automatically auto-populate data from month-wise GSTR-1 and GSTR-3B. It will be filed automatically after the due date is over.

GSTR-9C Reconciliation Statement

GSTR-9C is a reconciliation statement that is filed by entities falling under GST Audit that is having a turnover of more than 5 Crores. GSTR-9C must be certified by Chartered Accountant and Cost Accountant. The GSTR-9C contains two parts, one is regarding reconciliation and the other one is Certification. This statement acts as a base for the GST authorities to verify the correctness of the GST returns filed by the taxpayers. Any liability arising on account of non-reconciliation shall be paid in DRC-03. The due date of submitting GST-9C is the same as of GSTR-9.

GSTR-10 Final Return

A registered person whose registration has been canceled are required to Final return within 3 months of the date of cancellation or date of order of cancellation whichever is later.

GSTR-11 By Unique Identity Holders

Persons having a Unique Identity Number to claim a refund of taxes are required to file GSTR-11.

Frequently Asked Question (FAQs) regarding GST filing

GST Returns need to be mandatorily filed by all GST-registered persons. Normally, two GST returns GSTR-1 (GST returns for reporting outward supplies) and GSTR-3B (GST returns for payment of tax and claiming Input tax credit) are filed by newly registered persons.

GST Returns (GSTR-1 and GSTR-3B) will be compulsorily filed in case of zero sales of purchases. NIL GSTR-1 and GSTR-3B returns would be filed in those cases. In case the NIL return is not filed, late fees would be automatically levied by the GST portal and will be added to subsequent GST filing. Further, in case GST returns are not filed consecutively for six months, it may lead to suo moto GST cancellation.

GST returns (GSTR-1 and GSTR-3B) start from the day of the effective date of registration. The day GST is registered since returns are filed on monthly basis. GST returns start from that month only.

There are 25 GST returns generally to be filed annually, monthly GSTR-1 and GSTR-3B are filed along with an annual return. Further, for taxpayers who have opted for the QRMP scheme, the number of GST returns gets reduced however, tax liability remains the same. Further, in the case of e-commerce sellers whose TCS is collected by e-commerce operators. A TCS and TDS statement is filed along with GSTR-1 and GSTR-3B.

GST is divided into IGST, CGST, SGST, and UTGST. IGST means Integrated GST which is levied on inter-state sales. For instance, if Mr. A from Haryana sells goods to Mr. B from Uttar Pradesh. IGST would be levied by Mr. A as this is an interstate sale. CGST and SGST mean Central GST and State GST, which are levied for Intra state sales. For instance, if Mr. A from Haryana sells goods to Mr. B from Haryana only then it would be intra-state sales, and CGST and SGST would be levied. UTGST refers to Union Territory GST which is levied when sales are made to a person located in Union territories in India.

GST rates in India vary from categories of goods and services. GST slab rates are 3%, 5%, 6%, 12%, 18%, and 28%. The rates are revised from time to time on goods and services by the government.

GST is calculated on the taxable value of goods and services. Suppose, Mr. A sells goods worth INR 1,000 to Mr. B and the GST rate on such is 18%. INR 1,000 would be considered as taxable value and GST would be calculated with the formula GST Amount = Taxable Value * GST Rate. In the above example, GST would be calculated as follows, 1000*18% = INR 180, which needs to be collected from the customer first and then paid to the government by filing GST returns.

GST paid on purchases of goods that are used for further supply of goods and services can be claimed by the taxpayer. GST paid on purchases is required to be entered in the GSTR-3B return which should reconcile with GSTR-2B. After filing the GSTR-3B, the GST portion paid on the purchase of goods and services gets credited to the electronic credit ledger which can be further used to payment of output tax.

GSTR-2B is an auto-populated statement generated for the purchases made by the taxpayer. GSTR-2B reflects the total GST input credit to be claimed. The amount automatically gets transferred to GSTR-3B. GSTR-2B is populated on the basis of GSTR-1 filed by the supplier(sellers). The entire mechanism works in the following way. GSTR-1 is filed by the supplier adding the GSTIN of the purchaser before the 11th of the month and GSTR-2B is populated automatically on the basis of GSTR-1 filed by the supplier for the specific buyer before the 13th of the month.

The input tax credit in simple terms is the GST paid on the purchase of goods and services used for the furtherance of business.

A taxpayer who receives goods and services from the supplier needs to clear the payment made within 180 days of the invoice date. In case the taxpayer fails to pay for goods and services received within 180 days. GST input tax credit paid on such goods needs to be reversed in GSTR-3B. For instance, ABC Limited purchased goods worth INR 1,000 and paid INR 180 as GST in the month of April-22. INR 180 would be claimed by the taxpayer in April GSTR-3B, however, ABC Limited fails to pay the supplier within 180 days i.e. 1,180. GST input tax credit claimed in April GSTR-3B would now be required to reversed in GSTR-3B along with applicable interest.